Favorite Tips About When Should I Use Garch Halimbawa Ng Line Graph

:max_bytes(150000):strip_icc()/GARCH-9d737ade97834e6a92ebeae3b5543f22.png)

What Is The Garch Process? How It's Used In Different Forms Change Scale Excel To Add Horizontal Line Chart

What Are Arch & Garch Models Youtube Excel Pivot Chart Add Target Line Trend Model Types In Tableau

Ppt Week 10 Var And Garch Model Powerpoint Presentation, Free How To Make Scatter Plot With Multiple Lines In Excel Add A Line On An Graph

Garch Tutorial And Excel Spreadsheet 2016 Trendline Plotly Line Chart From Dataframe

![[PDF] The Use of GARCH Models in VaR Estimation Semantic Scholar](https://d3i71xaburhd42.cloudfront.net/5f2a00409f48ed4a596a36d6fdee3f82d8624f24/15-Table4-1.png)

[pdf] The Use Of Garch Models In Var Estimation Semantic Scholar Linear Regression Ti Nspire Cx Lines Ggplot

Ppt Module 3 Garch Models Powerpoint Presentation, Free Download Id How To Make A Supply And Demand Graph Combo In Excel

But then how do you determine the order.

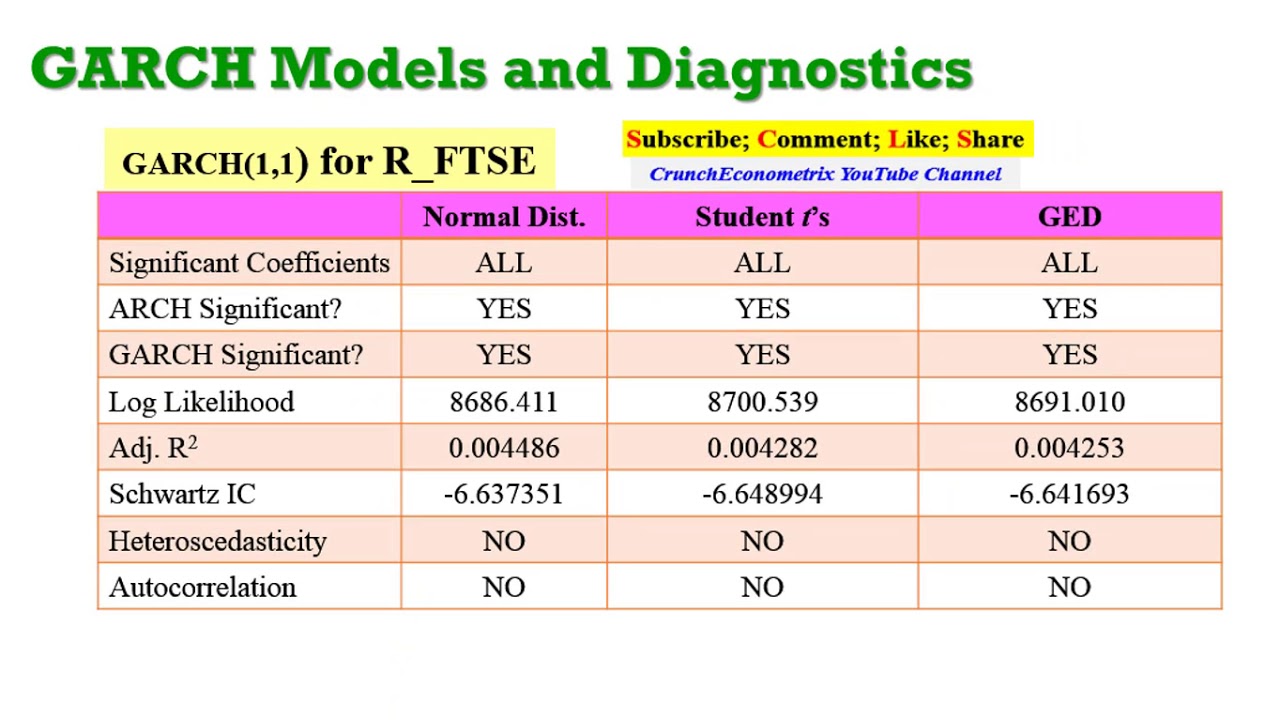

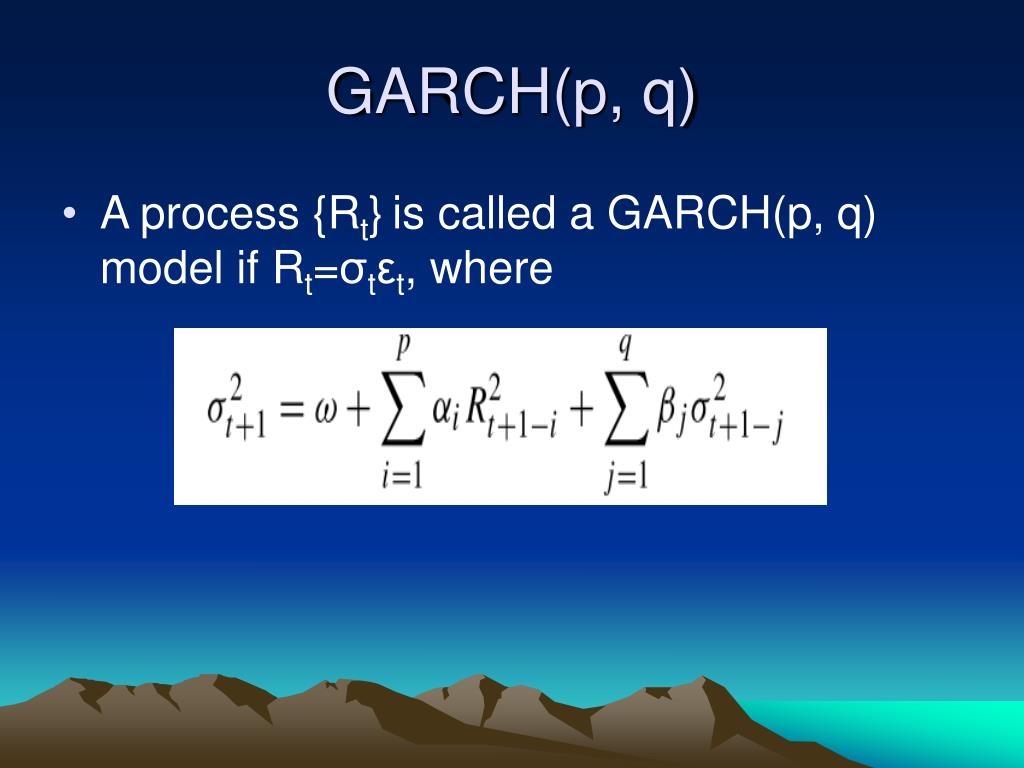

When should i use garch. If you are predicting with a time horizon of a month or more, then i’d be shocked if you got much value from a garch model versus a more mundane model. The reason why garch is useful is because it may better explain the volatility of certain series, particularly in finance. For instance, look at the graph below.

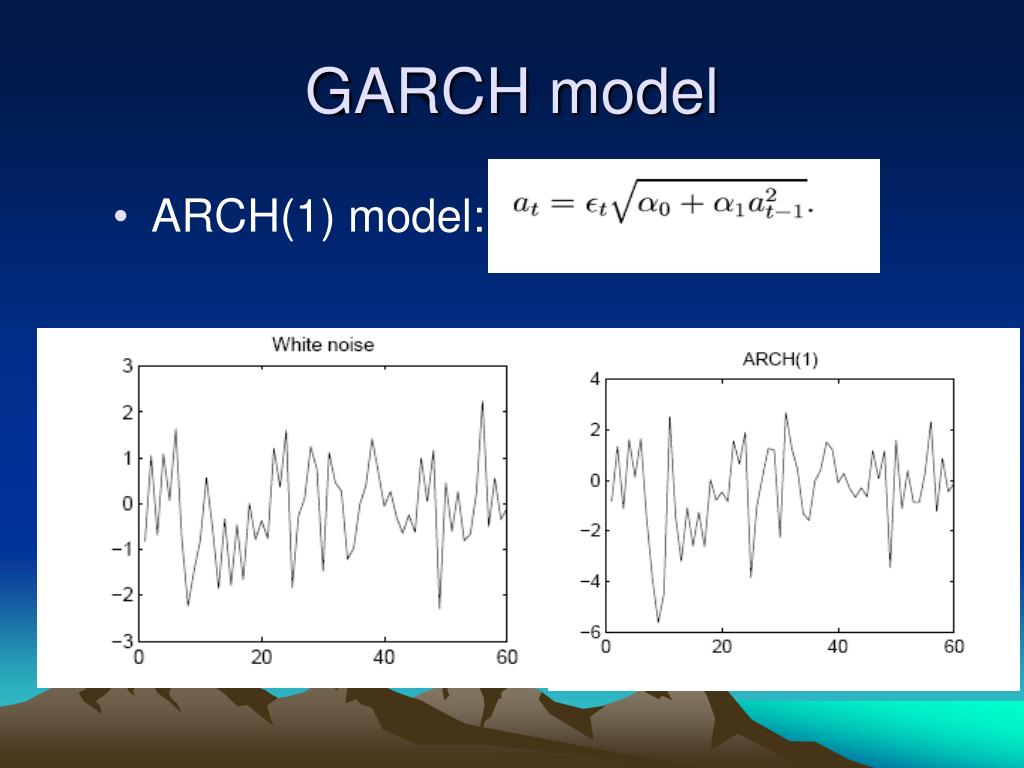

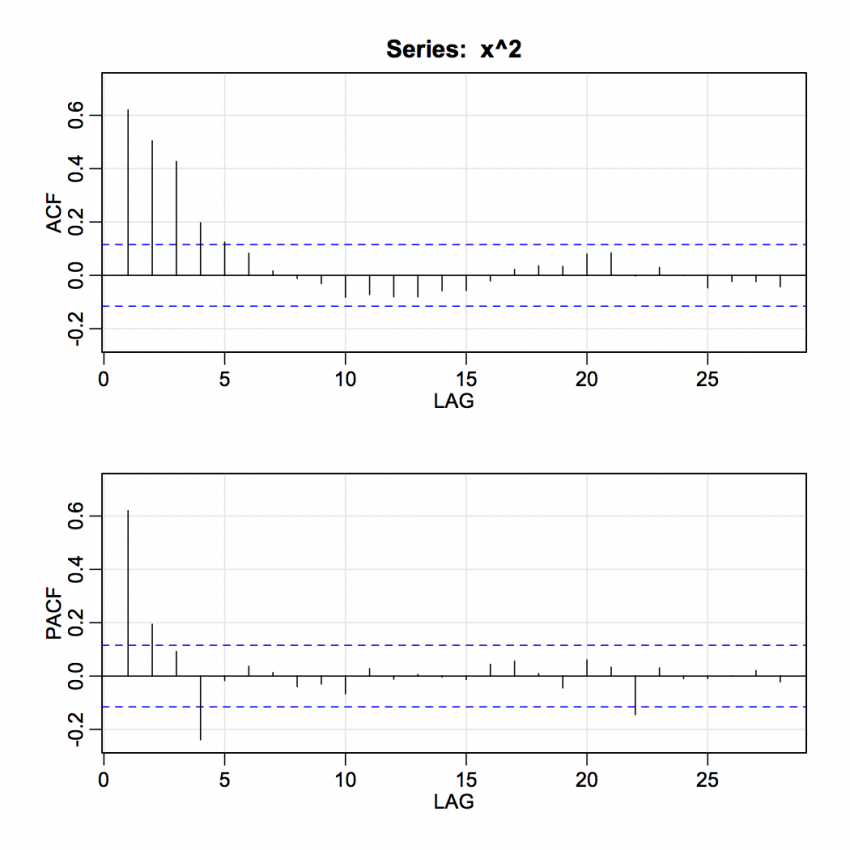

In order to model time series with garch models in r, you first determine the ar order and the ma order using acf and pacf plots. However, the nearly integrated behaviour of the conditional variance. If an autoregressive moving average (arma) model is.

For simplicity and illustration we will use a garch(1,1) model before assessing and testing different specifications. You cannot know which model is preferred before you learn some characteristics of your data. Arch and garch models can generate accurate forecasts of future daily return volatility, especially over short horizons, and these forecasts will eventually converge to.

Arch and garch models have become important tools in the analysis of time series data, particularly in financial applications. A dose of methadone being dispensed at a clinic in rossville, ga. Its provisions typically bind the shareholders to make certain.

Indeed, if the price is divided by $2$ at a certain point in time, it'd give a return of $. The arch model is appropriate when the error variance in a time series follows an autoregressive (ar) model; To get basic standard addiction treatment, americans should move to canada.

Financial professionals prefer garch for its realistic volatility prediction in diverse market conditions. Depends on what you're trying to do. If you are predicting a few days ahead, then garch should be quite useful.

(adobe stock) gone are the days when a. In addition, if you fit a garch model with raw log returns, then you're also implicitly assuming the mean is zero. Picking up the phone and calling your employer to let them know you are unwell and unable to work is a considerate approach.

The garch model is the most used technique for forecasting conditional volatility. Modeling daily returns is most useful for short term risk analysis of assets and portfolios using volatility and var. These models are especially useful when the goal of the study is to analyze and forecast volatility.

A shareholder agreement (sa) is a legally enforceable contract signed by large shareholders. Cer model captures most stylized facts of. I use a standard garch model:

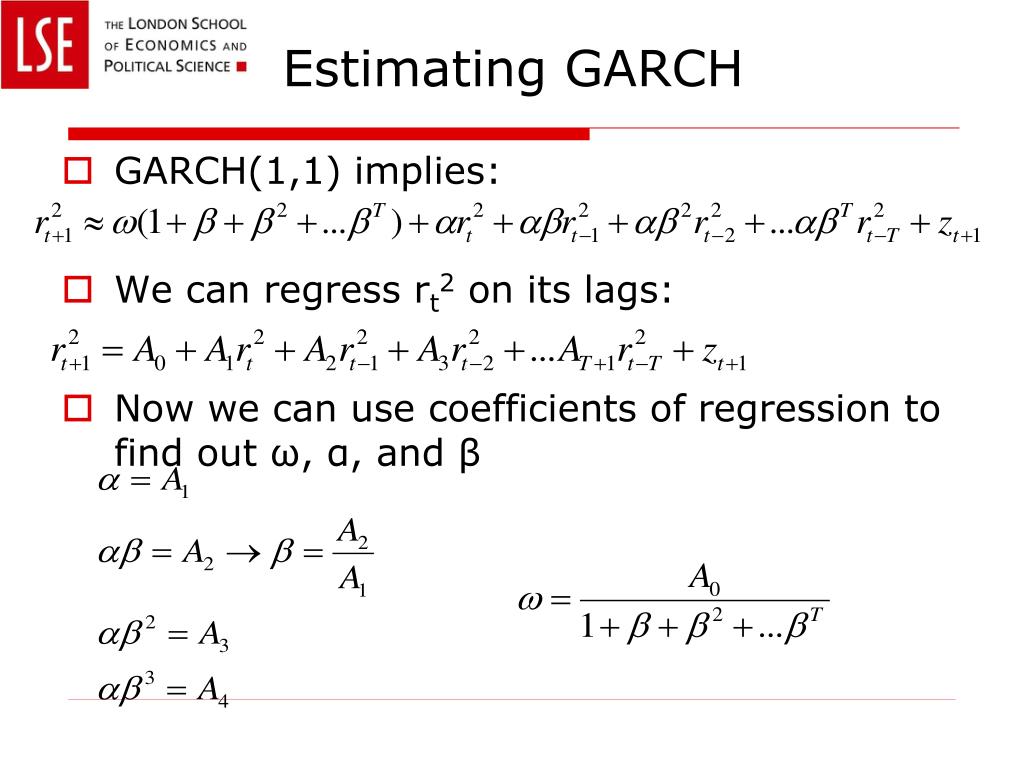

We will more formally test these effects. The garch updating formula takes the weighted average of the unconditional variance, the squared residual for the first observation and the starting variance and estimates. Garch models are not especially close to perfect.

Understanding The Garch Model In Python Online Xy Graph Maker Best Trend Line

Ppt Garch And Var Powerpoint Presentation, Free Download Id6961496 Ggplot2 Dashed Line How To Add Leader Lines In Excel Chart

Ppt Week 10 Var And Garch Model Powerpoint Presentation, Free How To Find A Specific Point On An Excel Graph Multiple Lines Ggplot2

Ppt Garch Models And Asymmetric Powerpoint Presentation Horizontal To Vertical In Excel Chart Online Draw

Ppt Garch And Var Powerpoint Presentation, Free Download Id6961496 Chartjs Line Chart Straight Lines 2 Graphs In One Excel

11.1 Arch/garch Models Stat 510 Linear Regression Chart In Excel How To Add Upper Limit Line Graph

Shishir Shakya's Blog Generalized Autoregressive Conditional Excel Two Y Axis What Is The X In

Ppt Garch And Var Powerpoint Presentation, Free Download Id6961496 Tableau Show Points On Line Making A Graph In Google Sheets

Garch 101 The Use Of Arch / Models In Applied Econometrics Plot Best Fit Line Excel Axes Symmetry Formula

Ppt Week 10 Var And Garch Model Powerpoint Presentation, Free Bell Curve Graph Creator Excel Data Horizontal To Vertical

Ppt The Garch Model And Their Applications To Var Powerpoint How Create Multiple Line Graphs In Excel Make A Single Graph

Ppt Garch Models And Asymmetric Powerpoint Presentation Excel Trendline For Part Of Graph How To Supply Demand In

Ppt Garch Models And Asymmetric Powerpoint Presentation How To Plot Demand Curve In Excel Trendline Formula

Ppt Garch And Var Powerpoint Presentation, Free Download Id6961496 Geom_point Geom_line A Velocity Time Graph

(eviews10) How To Estimate Exponential Garch Models Garchm Tgarch Tableau Grid Lines Excel Change Axis

Generalized Autoregressive Conditional Heteroskedasticity (garch Graph X 3 On A Number Line Add Trendline In Power Bi

Garch Process Awesomefintech Blog How To Draw Economic Graphs In Excel Geom_line Ggplot

Candlefocus Financial Terms & Glossary "garch Model An Overview Of Change Chart To Line Add Excel Bar